Poor Fundamentals

拙いファンダメンタルズ 19/6/6

豪ドル・円 FX のファンダメンタルズを19/5/26日に書きました。

5/26日時点で、利下げ時想定値を拙いファンダメンタルズ 19/5/26 のなかで

:

80%位は既に織り込まれているので、「知ったら終い」の可能性もあります。

5/18日安値 75.322円

1/ 4 日安値 75.241円

あたりまでの下落が見込まれます。

:

と予測しました。

その結果について考察していきます。

RBAの声明

2019/6/4(火)13:30

豪準備銀行は政策金利を発表しました。

大方の予想通り、6/4日には政策金利が 1.5% から 1.25% に引き下げられました。

声明文について英文も合わせて掲載しましたので、ニアンスも含め読み取っていただけると思います。

知事 Philip Loweによる メディア 発表声明

金融政策決定

番号 2019-15

日付 2019年6月4日

本日の会議で、理事会はキャッシュレートを25bp(0.25%)下げて1.25%にすることを決定しました。

当審議会は、雇用の成長を支援し、インフレが中期目標に一致する確信を高めるためにこの決定を下した。

世界経済の見通しは依然として堅調ですが、貿易紛争から生じる下振れリスクは高まっています。

国際貿易の成長は依然として弱いままであり、不確実性の増大は多くの国で投資意欲に影響を及ぼしています。

中国では、当局は金融システムのリスクに対処しながら、経済を支援するための措置を講じました。

ほとんどの先進国では、インフレは引き続き抑制されており、失業率は低く、賃金の伸びは回復しています。

世界的な財政状況は依然として緩和的です。

長期債券利回りとリスクプレミアム(期待収益率)は低いです。

オーストラリアでは、長期債券利回りは歴史的に低い水準にあります。

銀行の資金調達コストもさらに減少しており、マネーマーケットのスプレッドは昨年の増加を完全に覆した。

オーストラリアドルはここ数ヶ月間で少し下落しており、最近の狭い範囲での最低値にあります。

オーストラリア経済が2019年と2020年比較で約2.75%成長するという中心的なシナリオは残っています。

この見通しは、インフラ投資の増加とオーストラリアの輸出額における一部の資源部門の活動の回復によって支えられています。

国内の主な不確実性は引き続き、家計消費の見通しであり、

これは長期にわたる低所得成長と住宅価格の下落の影響を受けています。

家計の可処分所得の増加がある程度回復すると予想され、これが消費を支えるはずです。

昨年の雇用の伸びは堅調で、労働力の参加も増えており、失業率は依然として高いままで、

一部の地域では(労働者の)スキル不足の報告があります。

これらの動きにもかかわらず、最近の労働市場ではさらなる雇用の増大はほとんど見られない。

失業率は数ヶ月間 5%前後で安定していましたが、4月には5.2%まで上昇しました。

過去1年ほどの間の力強い雇用の伸びは、民間部門における賃金の伸びを回復させたが、全体的な賃金の伸びは低いままである。

賃金の伸びがさらに緩やかに上昇することが予想され、これは歓迎すべき発展となるでしょう。

まとめると、これらの労働市場の結果は、オーストラリア経済がより低い失業率を維持できることを示唆しています。

最近のインフレの結果は予想よりも低くなっており、多くの経済でインフレ圧力が弱まっていることを示唆しています。

しかしインフレは依然として回復すると予想されており、6月四半期にはガソリン価格の上昇により後押しされるでしょう。

今年の中心的シナリオは、基礎インフレ率が今年の1.75%、2020年には2%、その後はやや高くなるというものです。

一部の都市では、価格の大幅な上昇を受けて、既存の住宅市場の調整が続いています。

一部の市場では価格下落の速度が鈍化し、オークションのクリアランスレート(在庫処分率)が上がっていますが、状況は依然として軟調です。

住宅融資の伸びも最近安定している。

与信状況は厳しさを増し、投資家による与信に対する需要はしばらくの間抑制されています。

住宅ローン金利は依然として低いままであり、信用力の高い借り手にとっては強い競争力があります。※1)

政策金利を引き下げるという本日の決定は、経済の進展に寄与するのに役立ちます。

それは失業の減少をより早くし、インフレ目標に向けてより確実な進歩を達成するでしょう。

Media Release Statement by Philip Lowe, Governor:

4 June 2019

At its meeting today, the Board decided to lower the cash rate by 25 basis points to 1.25 per cent.

The Board took this decision to support employment growth and provide greater confidence

that inflation will be consistent with the medium-term target.

The outlook for the global economy remains reasonable,

although the downside risks stemming from the trade disputes have increased.

Growth in international trade remains weak and the increased uncertainty

is affecting investment intentions in a number of countries.

In China, the authorities have taken steps to support the economy,

while addressing risks in the financial system.

In most advanced economies, inflation remains subdued, unemployment rates

are low and wages growth has picked up.

Global financial conditions remain accommodative.

Long-term bond yields and risk premiums are low.

In Australia, long-term bond yields are at historically low levels.

Bank funding costs have also declined further,

with money-market spreads having fully reversed the increases that took place last year.

The Australian dollar has depreciated a little over the past few months

and is at the low end of its narrow range of recent times.

The central scenario remains for the Australian economy to grow by around 2¾ per cent in 2019 and 2020.

This outlook is supported by increased investment in infrastructure and a pick-up in activity in the resources sector,

partly in response to an increase in the prices of Australia's exports.

The main domestic uncertainty continues to be the outlook for household consumption,

which is being affected by a protracted period of low income growth and declining housing prices.

Some pick-up in growth in household disposable income is expected and this should support consumption.

Employment growth has been strong over the past year, labour force participation has been increasing,

the vacancy rate remains high and there are reports of skills shortages in some areas.

Despite these developments, there has been little further inroads into the spare capacity in the labour market of late.

The unemployment rate had been steady at around 5 per cent for some months,

but ticked up to 5.2 per cent in April.

The strong employment growth over the past year or so has led to a pick-up in wages growth in the private sector,

although overall wages growth remains low.

A further gradual lift in wages growth is expected and this would be a welcome development.

Taken together, these labour market outcomes suggest that the Australian economy can sustain a lower rate of unemployment.

The recent inflation outcomes have been lower than expected and suggest subdued inflationary pressures across much of the economy.

Inflation is still however anticipated to pick up, and will be boosted in the June quarter by increases in petrol prices.

The central scenario remains for underlying inflation to be 1¾ per cent this year, 2 per cent in 2020 and a little higher after that.

The adjustment in established housing markets is continuing, after the earlier large run-up in prices in some cities.

Conditions remain soft, although in some markets the rate of price decline has slowed and auction clearance rates have increased.

Growth in housing credit has also stabilised recently.

Credit conditions have been tightened and the demand for credit by investors has been subdued for some time.

Mortgage rates remain low and there is strong competition for borrowers of high credit quality. ※1)

Today's decision to lower the cash rate will help make further inroads into the spare capacity in the economy.

It will assist with faster progress in reducing unemployment and achieve more assured progress towards the inflation target.

The Board will continue to monitor developments in the labour market closely and

adjust monetary policy to support sustainable growth in the economy and

the achievement of the inflation target over time.

※1)

この部分は英文を見ても理解しずらい。

豪の不動産価格事情を理解する必要があるようです。

丁寧に翻訳すると以下のようになると考えられます。

不動産価格の下落により、銀行の貸渋りや厳しい条件でローンを借りられる人が少ないため、資金に余裕のある投資家のみが投資を続けている。

RBA 追加コメント

金利はさらに引き下げられるか?-の部分を抽出

総裁)フィリップロウ

リザーブバンクボードディナーシドニー

2019年6月4日

https://www.rba.gov.au/speeches/2019/sp-gov-2019-06-04.html

(この URL にはなかなかうまくアクセスできません)

これは私に二つ目の質問をもたらします:金利はさらに引き下げられるのでしょうか?

ここでの答えは、取締役会はまだ決定を下していないということですが、低いキャッシュレートを期待するのは不合理ではありません。

RBA の最新の予測は、キャッシュレートが市場価格設定に含まれる過程をたどると仮定して作成されています。

それは、年末までにキャッシュレートが約1%になるというものでした。

もちろん、他にもさまざまなシナリオが考えられ、その証拠がどのように展開されるか、特に労働市場に大きく左右されます。

オーストラリアで持続的に低い失業率が達成可能であるという議論にあなたが同意するならば、我々全員が考えるべきである質問は:

どうやってそこに着くのか?

現在のポリシー設定で十分である可能性があります

- 私たちはただ我慢する必要があるということです。

しかし、現在の政策設定が私たちの我慢を短くする可能性もあります。

これを考えると、より低い金利の可能性はテーブルに残る。

金融政策には重要な役割があり、必要に応じてその役割を果たすことができます。

それを言って、私はまた、金融政策が唯一の選択肢ではないことを認識したいと思います。

金融政策だけに頼ることにはいくつかのマイナス面があり、現実的に達成できることには限界があります。

ですから、国として、私たちは失業を減らすための他の選択肢にも注目すべきです。

1つの選択肢は、インフラへの支出などによる財政支援です。

この支出は経済の需要を増大させるだけでなく、経済の生産能力も増大させます。

そのため、需要側と供給側の両方で機能します。

もう1つの選択肢は、企業の拡大、投資、革新、そして人々の雇用を支援する構造的政策です。

3つの選択肢(金融政策 + 財政支援 + 構造的政策)すべてについて考える価値があります。

私の考えでは、最善の選択肢は、企業の拡大、投資、革新、そして雇用を支援する構造的政策です。

力強いダイナミックなビジネスセクター(活動分野)は、雇用を創出するための最良の方法です。

構造的政策は雇用創出に役立つだけでなく、私たちの生活水準を向上させる主な原因である生産性の向上を促進するのにも役立ちます。

ですから、国として、私たちがこれに集中し続けることが重要です。

This brings me to the second question: are interest rates going to be reduced further?

The answer here is that the Board has not yet made a decision,

but it is not unreasonable to expect a lower cash rate.

Our latest set of forecasts were prepared on the assumption that the cash rate would follow the path implied by market pricing,

which was for the cash rate to be around 1 per cent by the end of the year.

There are, of course, a range of other possible scenarios and much will depend on how the evidence evolves,

especially on the labour market.

Our latest set of forecasts were prepared on the assumption that the cash rate would follow the path implied by market pricing,

which was for the cash rate to be around 1 per cent by the end of the year.

There are, of course, a range of other possible scenarios and much will depend on how the evidence evolves,

especially on the labour market.

If you accept the argument that a sustainably lower rate of unemployment in Australia is achievable,

the question that we should all be thinking about is:

how do we get there?

It is possible that the current policy settings will be enough

– that we just need to be patient.

But it is also possible that the current policy settings will leave us short.

Given this, the possibility of lower interest rates remains on the table.

Monetary policy does have an important role to play

and we have the capacity to play that role if needed.

In saying that, I also want to recognise that monetary policy is not the only option.

There are certain downsides from relying just on monetary policy

and there are limitations on what, realistically, can be achieved.

So, as a country, we should also be looking at other options to reduce unemployment.

One option is for fiscal support, including through spending on infrastructure.

This spending not only adds to demand in the economy,

but it also adds to the economy's productive capacity.

So it works on both the demand and supply side.

Another option is structural policies that support firms expanding, investing, innovating and

employing people.

All three options are worth thinking about.

From my perspective, the best option is the third one

– structural policies that support firms expanding, investing, innovating and employing people.

A strong dynamic business sector is the best way of creating jobs.

Structural policies not only help with job creation,

but they can also help drive the productivity growth

that is the main source of improvement in our living standards.

So, as a country, it is important that we keep focused on this.

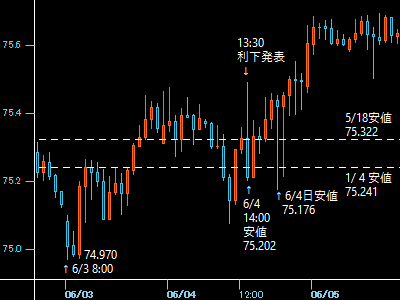

利下結果

大方の予想通り、6/4日には政策金利が 1.5% から 1.25% に引き下げられました。

その時の豪ドル/円の値動きを下図に示します。

2019/6/4日 豪ドル/円 1時間足

拙いファンダメンタルズ 19/5/26のなかで述べた

「知ったら終い」

5/18日安値 75.322円

1/ 4 日安値 75.241円

までの下落予測通り

結果は

6/4日安値 75.176円

となりました。

予測値は少し高めでしたが、まずは正しく予測できたかなと思います。

今後

声明、コメントを読むと、

「市場は年末までに金利を1.0%にすると予測しているようだが、そんなことはない、

インフラ投資や構造改革を進めるので、今回の利下げだけで当分は大丈夫」

と主張しているように思えます。

年内は利下げはないと解釈してよさそうです。

よって、

6/3 安値 74.970 円

が底値となったとみてよいようです。

RBA ウェブサイト

話は少し脱線しますが、RBA のウェブサイトは

http://www.rba.gov.au/

にあります。

もちろん英語のサイト。

政策金利発表日等はアクセス制限がかかります。

このアクセス制限なかなか解除されません。

1~2週間ぐらいは見えないようです。

でも

RBA 日本語サイト

に行くと日本語版があります。

ただ、残念ながらちょっと違和感があります。

完全な日本語とは言い難い。

日本語ページは、元の場所からセキュリティで保護された接続を使用せずに取得されますので、

英語版がセキュリティ保護されても閲覧することができます。

日本人しか見ないしアクセスがそれほど多くないため閲覧が比較的容易です。

でも翻訳するのに時間がかかるので反応が非常に遅いです。

RBA のサ-バは Poor Server です。

何とかしてもらいたいです。

拙いファンダメンタルズを最後までお読みいただきありがとうございます。

さてどうなるのか楽しみです。

拙いファンダメンタルズ 19/6/9 に進む

拙いファンダメンタルズ 19/5/26 に戻る